Скачать

Black-Scholes Equation from Ito's Lemma

Автор: Mike, the Mathematician

Загружено: 2023-01-31

Просмотров: 3823

Описание:

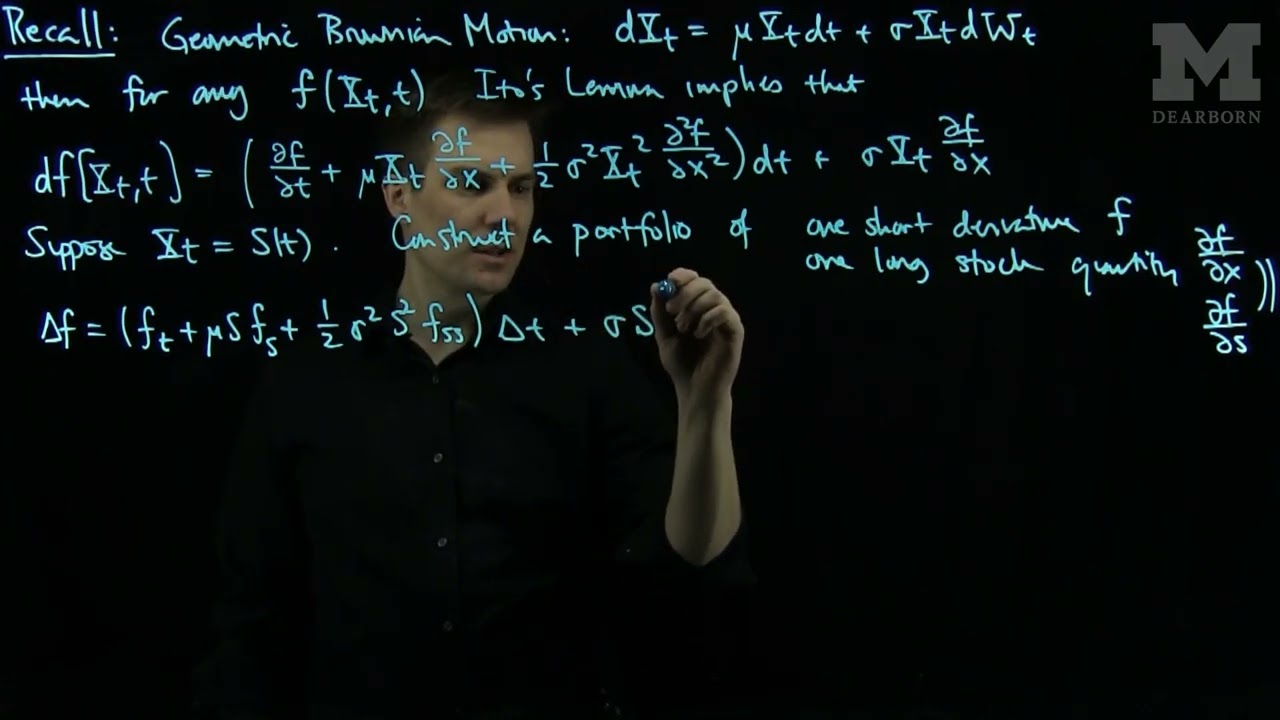

We derive the Black-Scholes equation from the Ito Lemma. We construct a portfolio which shorts one derivative and takes a long fractional position in the stock (which is the delta of the option). This portfolio will be risk free.

#mikedabkowski, #mikethemathematician, #profdabkowski, #mathfinance

Доступные форматы для скачивания:

Скачать видео mp4

-

Информация по загрузке: