Probabilistic Modeling - A Fairly Comprehensive Case Study

Автор: Analytics in Practice

Загружено: 2026-01-17

Просмотров: 58

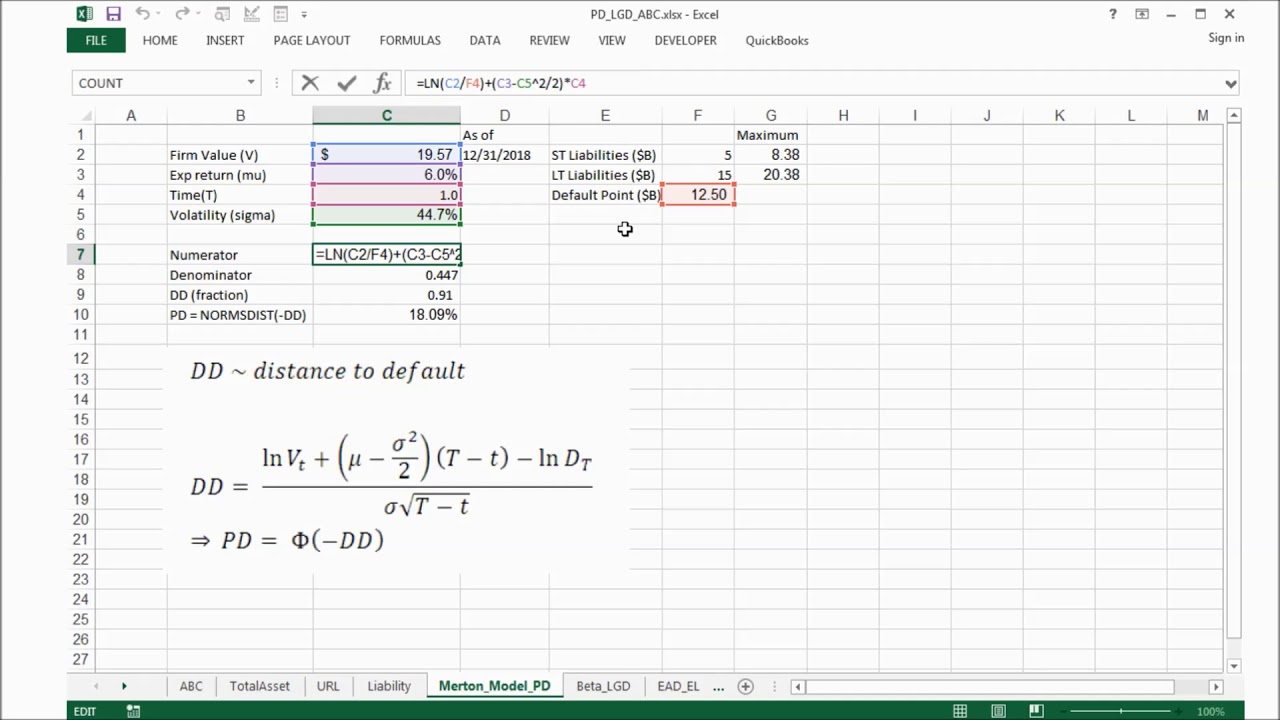

This case study explains probabilistic modeling as a practical way to represent uncertainty with probability distributions and then answer decision-focused questions using quantities like posterior probabilities, credible intervals, and risk metrics. It begins with a simple Bayesian Beta-Binomial example to estimate an uncertain rate (such as conversion or fraud rate), producing a posterior mean, a 95% credible interval, and probabilities of exceeding thresholds. The same Beta posterior approach is then applied to credit risk by modeling a segment’s default rate, estimating the posterior PD and computing the chance the PD exceeds a risk limit. Next, it introduces Monte Carlo loss simulation using a frequency–severity framework, where event counts follow a Poisson distribution and loss amounts follow a Lognormal distribution to generate annual loss distributions and compute AAL, VaR, TVaR, and the probability of any loss. The case study emphasizes that probabilistic modeling in practice means choosing a distributional “story” and using it to guide threshold decisions, quantify risk under stress, and minimize expected loss. It then shows fraud detection as an expected-loss thresholding policy, flagging transactions when expected fraud loss exceeds review cost and summarizing portfolio-level cost tradeoffs. A credit underwriting example combines posterior PD uncertainty with loan economics (LGD, EAD, interest profit) to estimate expected profit per loan and the probability of unprofitable outcomes. A pricing example models uncertain demand with elasticity and noise, uses Monte Carlo simulation across price points, and selects the price that maximizes expected profit while also examining downside and upside profit quantiles. Insurance claims reserving is modeled again with a Poisson–Lognormal frequency–severity setup including deductibles and limits to compute expected loss and capital metrics like VaR/TVaR. Finally, churn is treated as an uncertain rate updated with a Beta posterior and paired with retention offer economics to evaluate whether a retention strategy is expected to be profitable, and the study closes with market simulations using normal returns, bootstrap resampling for fat tails, and a volatility-based regime switch to better reflect real-world return behavior.

Доступные форматы для скачивания:

Скачать видео mp4

-

Информация по загрузке: