Johansen Cointegration Test: Choosing Between VAR and VECM Models

Автор: Umeh_richard Econometrics

Загружено: 2026-01-09

Просмотров: 17

In this video, I demonstrate how to use the Johansen cointegration test to determine whether to estimate a VAR or VECM model for your time-series data.

You will learn how to:

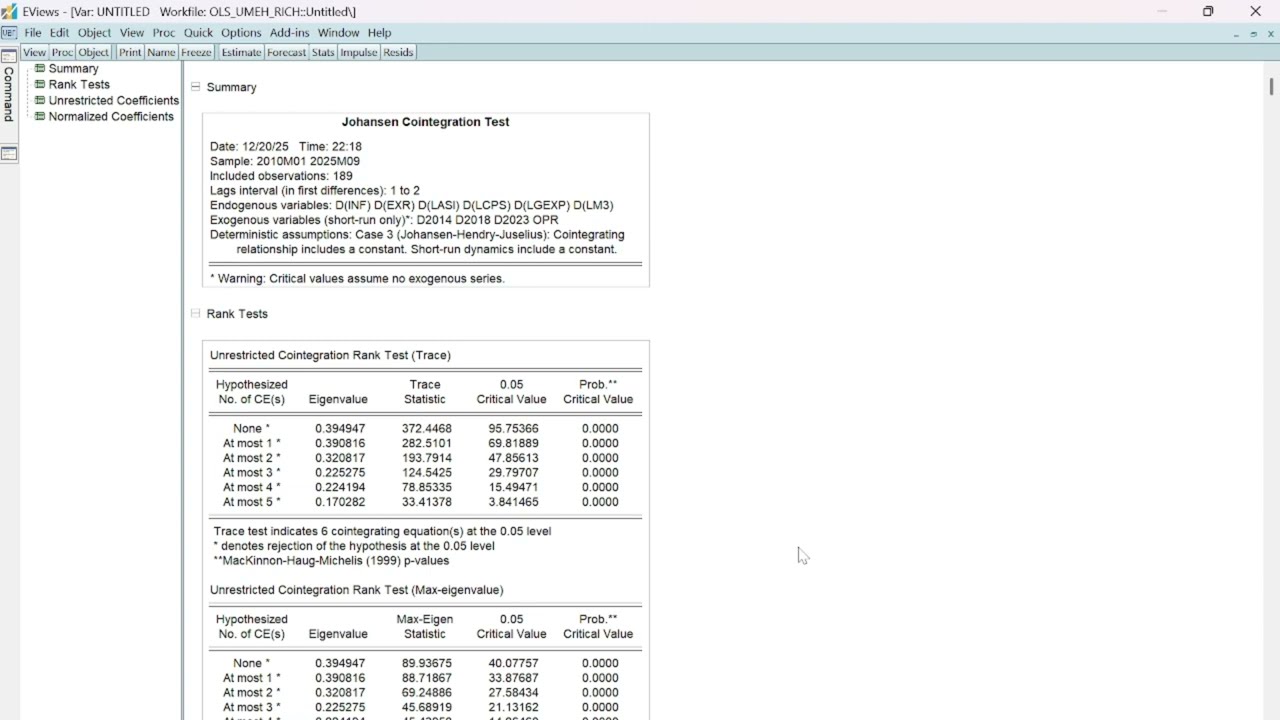

Perform the Johansen cointegration test step by step

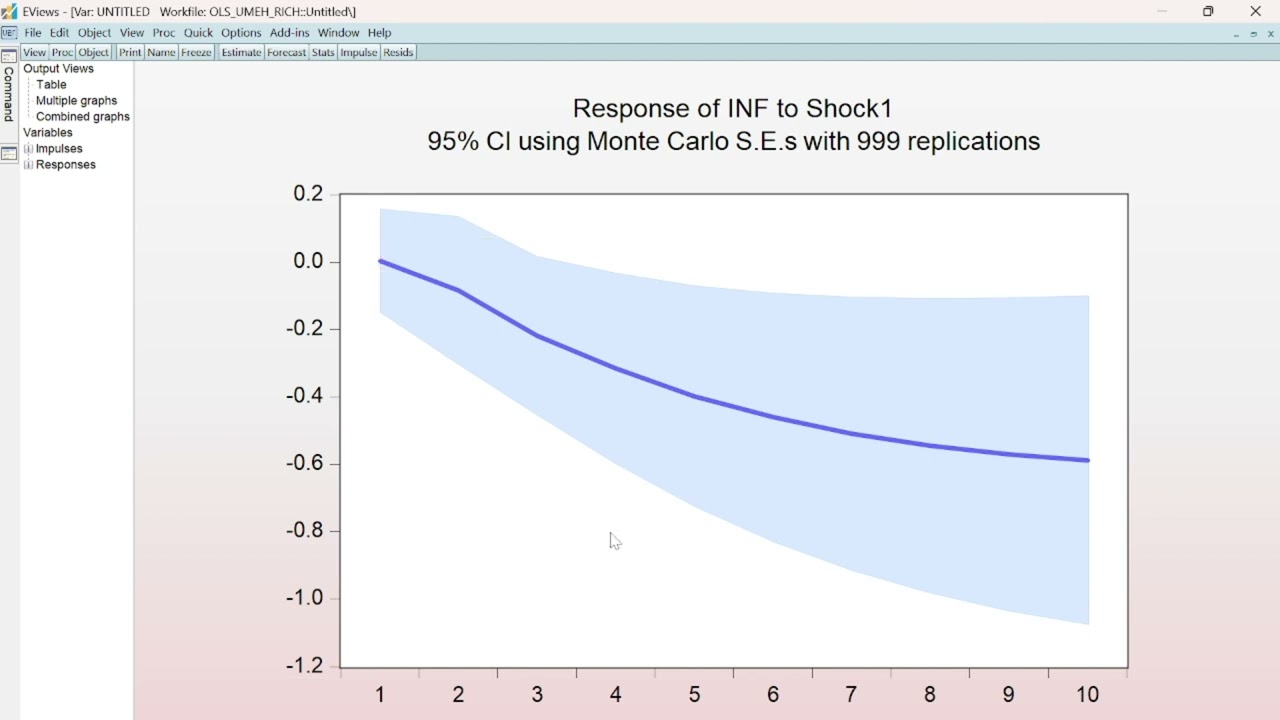

Interpret the trace and maximum eigenvalue statistics

Decide whether a VAR model or a VECM (Vector Error Correction Model) is appropriate based on cointegration results

Apply these techniques in economic research, thesis work, or policy-oriented studies

This tutorial is ideal for postgraduate students, researchers, economists, and data analysts working with time-series data in EViews or similar econometric software. By the end of this video, you’ll be able to choose the correct model for multivariate time-series analysis confidently.

📌 Topics Covered:

Johansen Cointegration Test Basics

VAR vs VECM Model Selection

Interpreting Cointegration Test Results

Practical Examples

👍 If you find this video helpful, please like, share, and subscribe for more tutorials on econometrics, time-series modeling, and applied economic research.

Доступные форматы для скачивания:

Скачать видео mp4

-

Информация по загрузке: