11. Time- and State-Dependent Resampling

Автор: Fortitudo Technologies

Загружено: 2025-04-19

Просмотров: 381

This is the twelfth video in the open-source fortitudo.tech Python package playlist: https://github.com/fortitudo-tech/for...

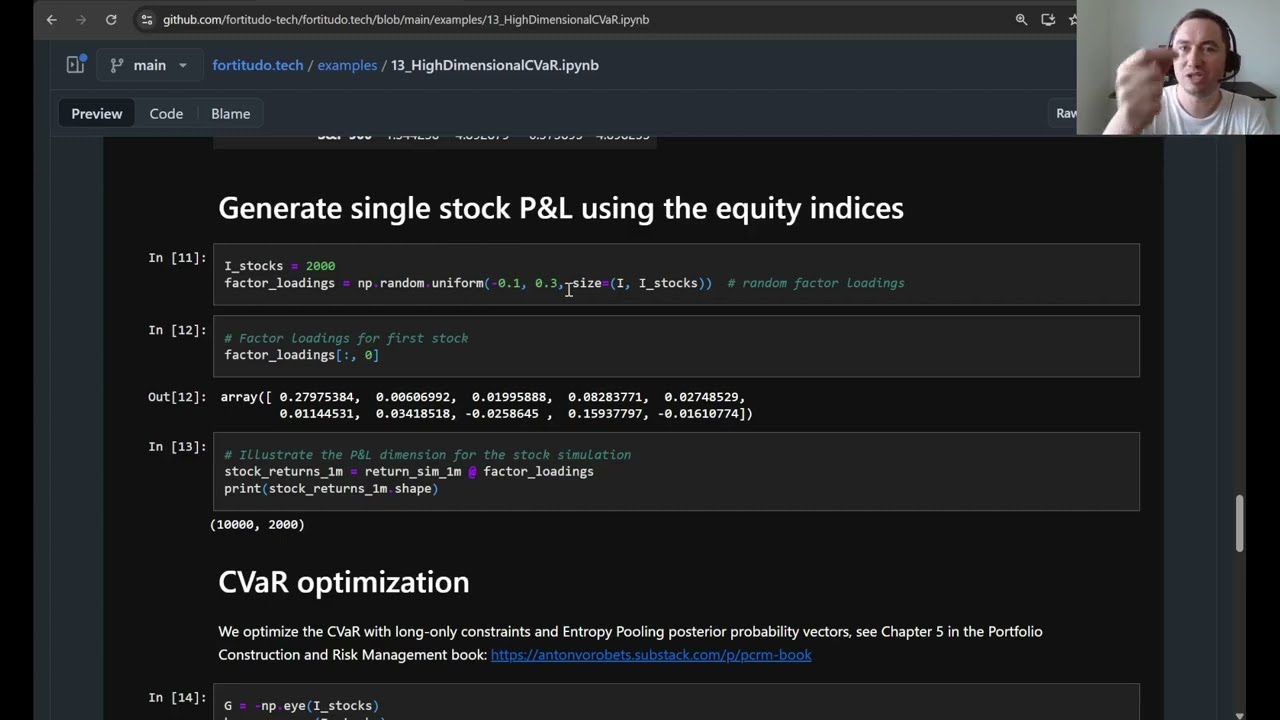

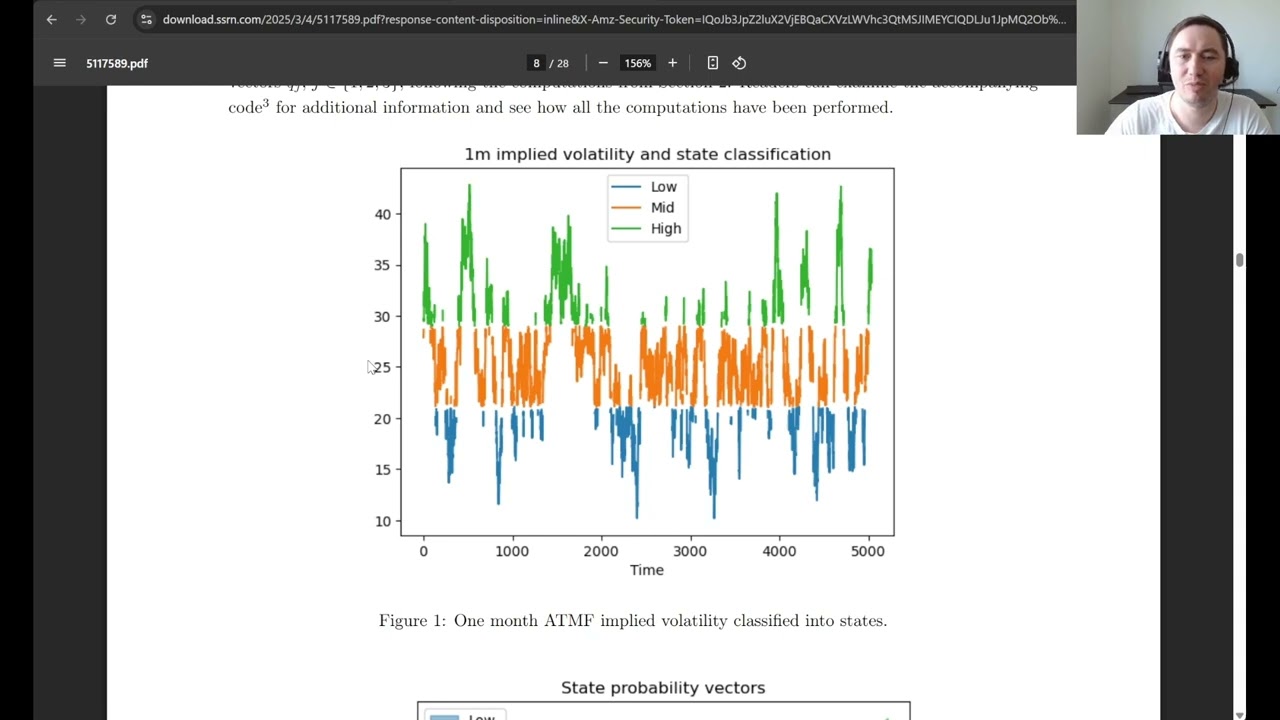

This video goes through the Time- and State-Dependent Resampling SSRN article available at https://ssrn.com/abstract=5117589

It also goes through the article's Python code available at https://github.com/fortitudo-tech/for...

Time- and State-Dependent Resampling is a new general class of time series resampling methods for high-dimensional investment market simulation.

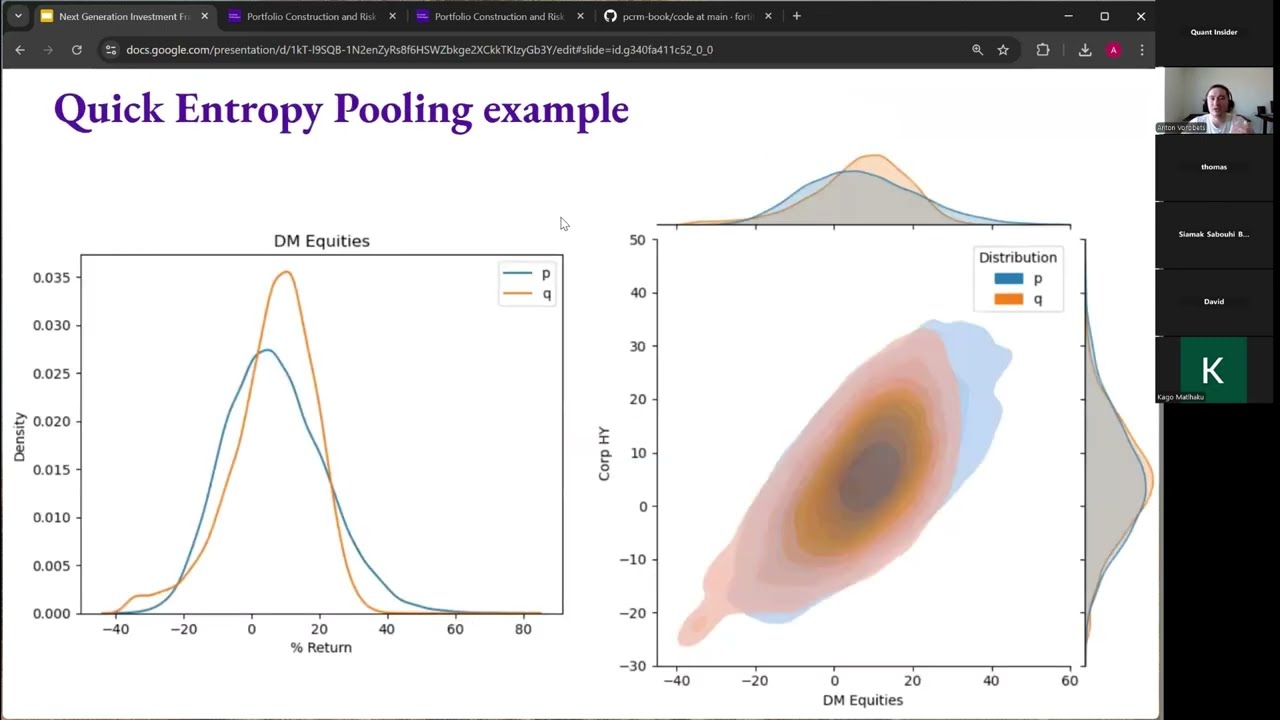

The Fully Flexible Resampling method, first introduced in Chapter 3 of the Portfolio Construction and Risk Management book (https://antonvorobets.substack.com/p/..., is an instance of the Time- and State-Dependent Resampling class.

You can read more about the relation between the Fully Flexible Resampling method and the Time- and State-Dependent Resampling class here: https://antonvorobets.substack.com/p/...

Доступные форматы для скачивания:

Скачать видео mp4

-

Информация по загрузке:

![Как происходит модернизация остаточных соединений [mHC]](https://imager.clipsaver.ru/jYn_1PpRzxI/max.jpg)