Скачать

R29 Intro to GARCH, Generalized Autoregressive Conditional Heteroskedasticity, , R and RStudio

Автор: Scott Burk

Загружено: 2019-01-20

Просмотров: 1234

Описание:

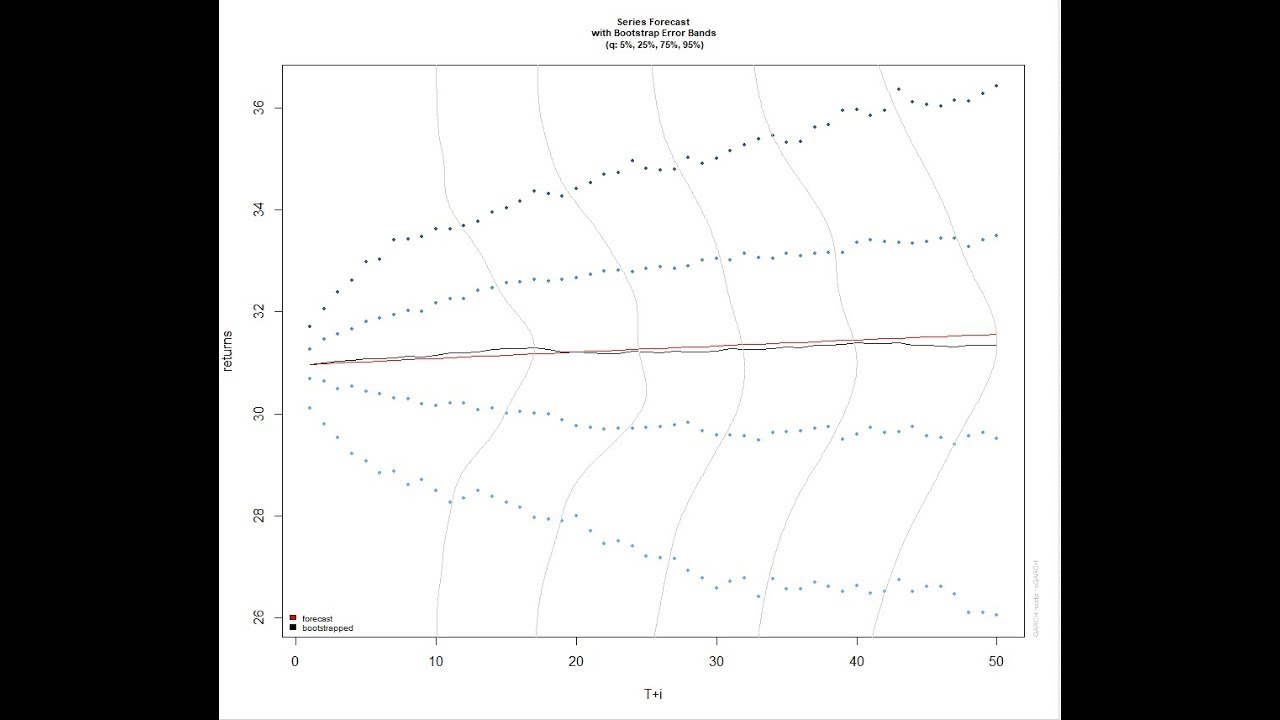

Basic Time Series Methods in R is part of a series of forecasting and time series videos. This short video covers a financial modeling and an introduction to GARCH, Generalized Autoregressive Conditional Heteroskedasticity. If you are interested in Forecasting and Time Series, you will want to subscribe to this series!

Доступные форматы для скачивания:

Скачать видео mp4

-

Информация по загрузке: