(EViews10):Discussing Results, VAR Models(2)

Автор: CrunchEconometrix

Загружено: 2018-03-20

Просмотров: 28519

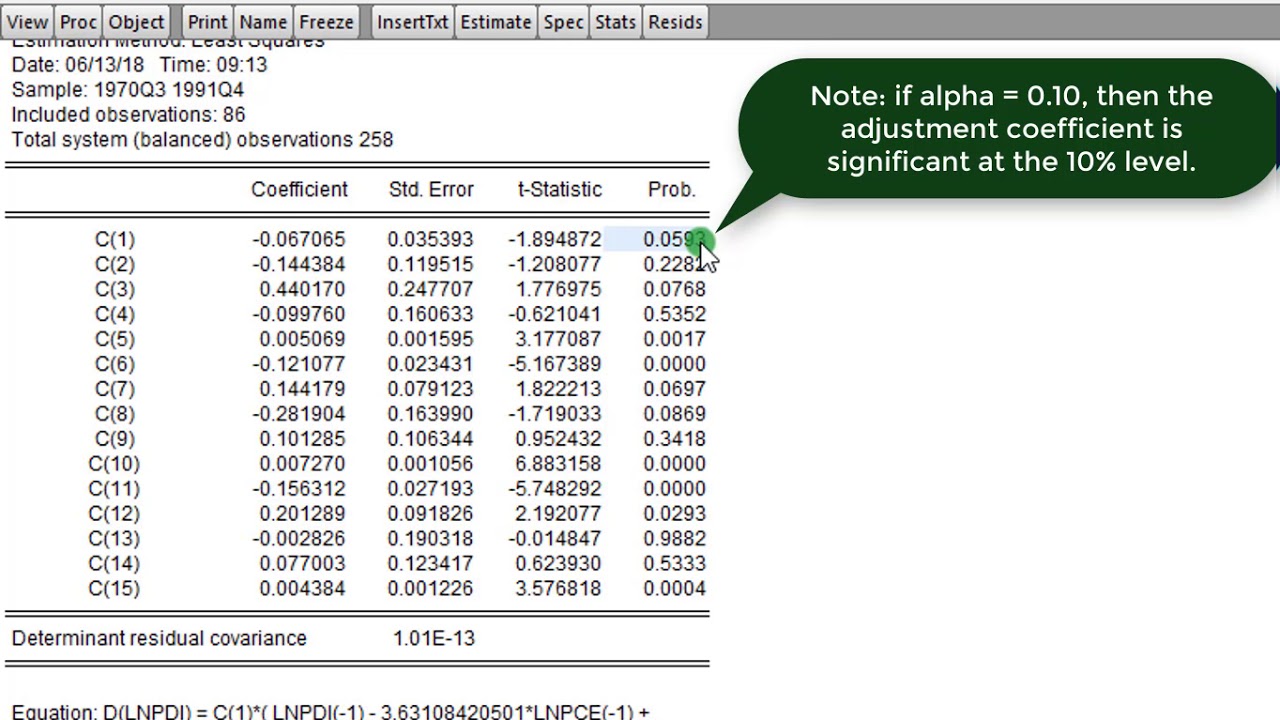

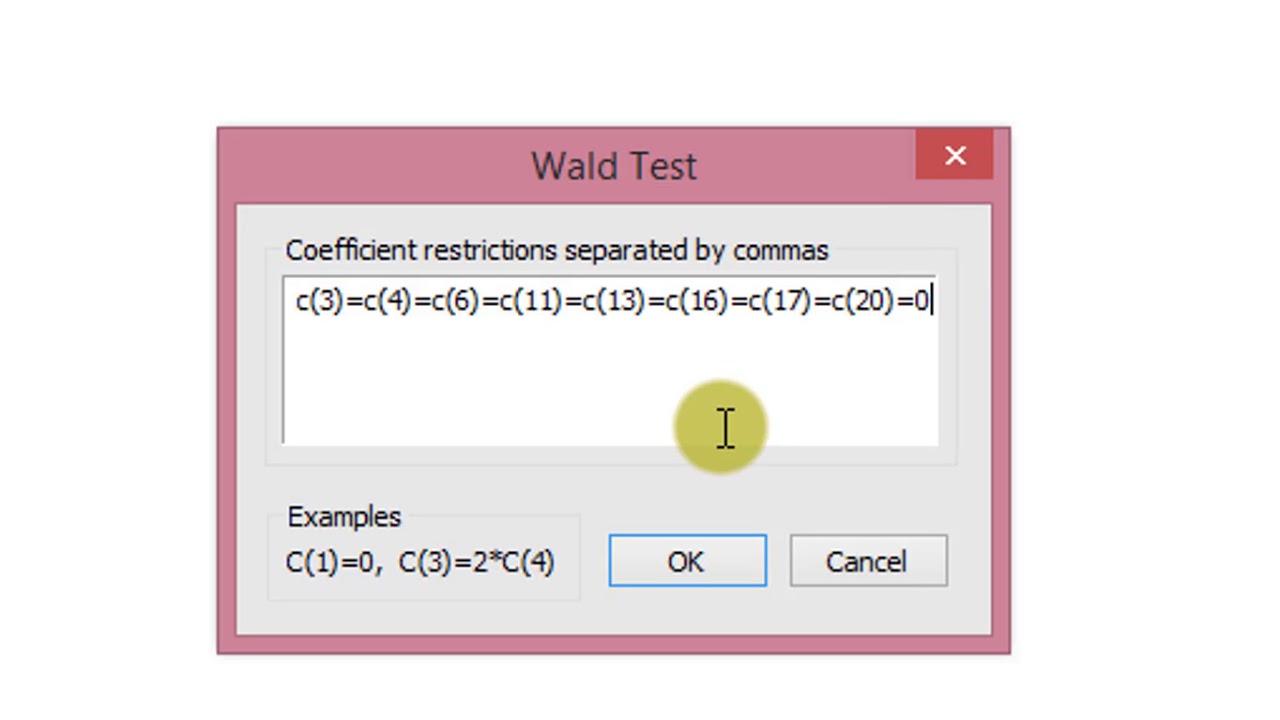

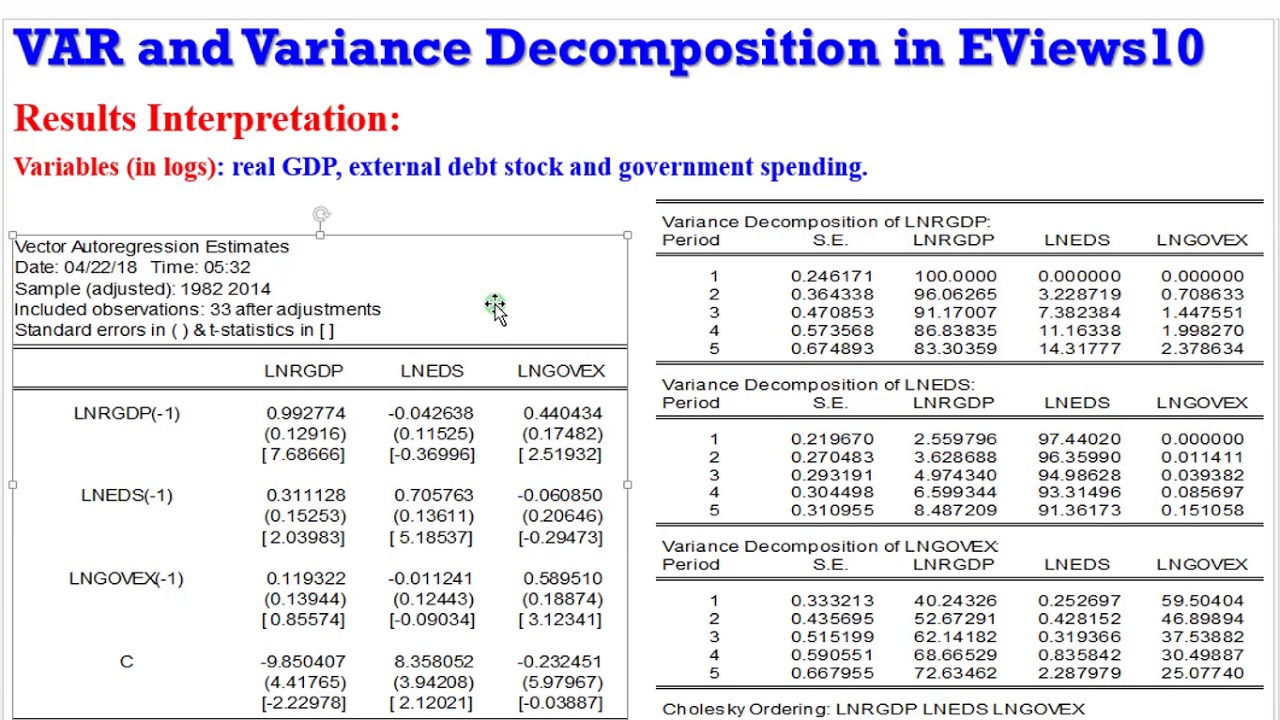

This video show how to discuss results from VAR models. After performing both stationarity and cointegration tests and you find that all the series are integrated of order one, the next thing to do is to construct a vector autoregression (VAR) model and estimate using the ordinary least squares (OLS) method. This hands-on tutorial teaches how to construct, estimate and discuss the results from a VAR model in EViews10.

Here is the link to the ex21-1.wf1 dataset (EViews file) used for this tutorial (endeavour to have a Google account for easy accessibility): https://drive.google.com/drive/u/1/fo...

Follow up with soft-notes and updates from CrunchEconometrix:

Website: http://cruncheconometrix.com.ng

Blog: https://cruncheconometrix.blogspot.co...

Forum: http://cruncheconometrix.com.ng/blog/...

Facebook: / cruncheconometrix

YouTube Custom URL: / cruncheconometrix

Stata Videos Playlist: • (Stata13):Estimate and Interpret Two-way A...

EViews Videos Playlist: • (EViews10):Interpret VECM, Forecast Error ...

Доступные форматы для скачивания:

Скачать видео mp4

-

Информация по загрузке: