WebeXions 2023 Oct - Employee Ownership Trusts (EOTs)

Автор: biz4Biz

Загружено: 2023-12-04

Просмотров: 57

In today's WebeXions Andrew will discuss Employee Ownership Trusts (EOTs).

A must watch for anyone in business, let alone those looking to make an exit or change the way their business is setup

Questions:

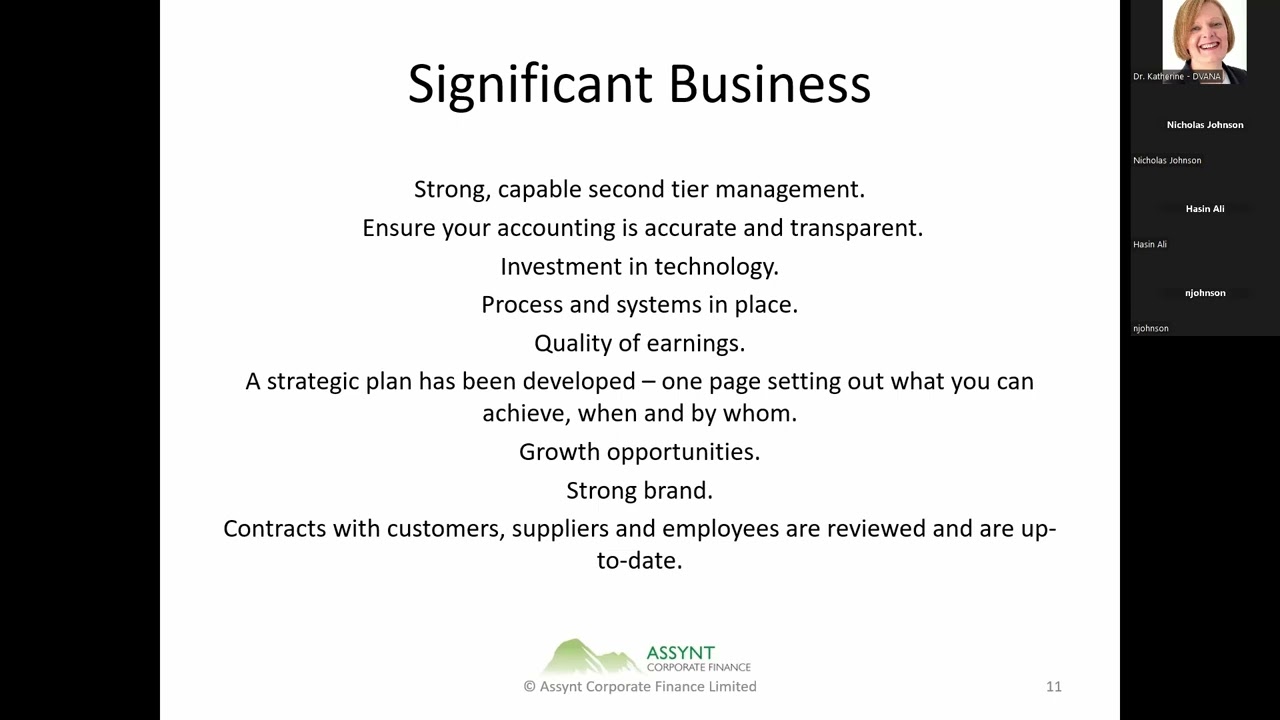

1. Andrew, you’ve covered some of the misconceptions, what are the other pitfalls and downsides?

Having cold feet during the process. That is, where a feasibility study comes in so the angles can be considered.

Overvaluation – owners need to be pragmatic about what is a reasonable pay down period for any loan.

It sounds exciting at first but if the (senior) employees change their minds it will take the whole shine off the process. Baxendale’s ought to be consulted after the feasibility study has confirmed it is reasonable and they can advise as to when and how employees should be handled and told; how communications and expectations ought to be handled.

2. Can shareholder employees receive the £3,600 bonus?

This is a complicated area. I will briefly explain. The number of employees (and their associates – I’ll not define for now) cannot exceed 40% of the total of participants and employees.

So, if there are 25 employees in the company provided the employees concerned are below 10 then okay, they can receive the bonus.

If 10 employees in the company and they are more than 4 then they are not okay to receive the bonus.

3. What happens to an existing bonus scheme for employees after the sale?

If there is one in existence before completion, then it can continue.

4. Do all the shares have to be sold?

In a word “No”. So long as the trust has enough shares, then existing shareholder(s) can retain their shares. They will of course be in a minority. They can of course sell their shares at a later date. However, if they do this, they could forfeit the 100% tax relief as it is only available when the initial shares are sold to the trust. Any further sales will be subject to 10% capital gains tax provided all the conditions are present.

5. Can shareholders take ad hoc and variable amounts of the debt?

Yes, but…. For example, you could reduce the loan by:

£50,000 in year 1

£nil in year 2

£nil in year 3

£150,000 in year 4

These arrangements will need to be set out in the Clearance Application to HMRC. They could be regarded as a means of extracting cash out of the company without paying any capital gains tax. So, I prefer a normal commercial loan arrangement since this is what they would expect.

6. What is the tax position of the EOT and the company?

The company remains a trading company and pays corporation tax as normal on its taxable profits. The monies paid across to the trust come out after taxed income and there is no further tax on the monies paid as distributions to the trust.

There must therefore be distributable profits in the company, as defined by The Companies Act 2006.

The trustee company is not considered to be a trading company.

7. What view do the banks take on the funding of the outstanding consideration?

They tend to look at it along the lines of a management buyout except that the managers are not putting in any money. It has to be a bankable proposition and thus the repayments on existing borrowings are considered. There may be a case for going to the banks after say three or four years when the new structure has settled down and the company’s banker would consider taking on the existing loan relating to the outstanding consideration.

In any event, there is no harm in approaching the bank once the feasibility study has been completed.

8. Can the Company buy another business?

The short answer is yes. Just remember the trustees will need to be consulted and they will consider it if the proposal is in the best interests of the employees. Remember, the company will be repaying the loan for the outstanding consideration so any further borrowings, if required, will need to be considered too.

9. Contact details and other information can be found.

Website: www.assyntcf.co.uk

EOT Pages

What are EOTs https://www.assyntcf.co.uk/employee-o...

The Legal Bits https://www.assyntcf.co.uk/employee-o...

The tax incentives https://www.assyntcf.co.uk/employee-o...

Comparison between a trade sale and an EOT https://www.assyntcf.co.uk/comparing-...

Disclaimer The presentation is intended to promote discussion and debate and are not put forward by way of definitive advice and should not be relied upon without seeking further advice in relation to any specific matter. It is recommended you seek specialist advice, from Assynt Corporate Finance Limited or another suitably qualified professional adviser, in relation to any specific client matter. The law and HMRC practices are summarised as they are understood to have effect as at 1st May 2019.

Доступные форматы для скачивания:

Скачать видео mp4

-

Информация по загрузке: