Interest Rate Differentials and the USD/PYG Exchange Rate (Part 1) | Jose Aurelio Fiorio Weberhofer

Автор: José A. Fiorio Weberhofer – Finance & Economics

Загружено: 2026-01-03

Просмотров: 13

▶️ Continue with Part 2 (full series playlist):

• Плейлист

In this video, Jose Aurelio Fiorio Weberhofer presents an econometric analysis of the relationship between interest rate differentials and the USD/PYG exchange rate, continuing a series of applied macroeconomic studies on Paraguay.

This video builds on previous analyses published on this channel, particularly my earlier work on agricultural export prices and their impact on the Paraguayan Guaraní. While commodity prices capture the trade channel of exchange rate determination, this video focuses on the financial and monetary channel through interest rate differentials between Paraguay and the United States.

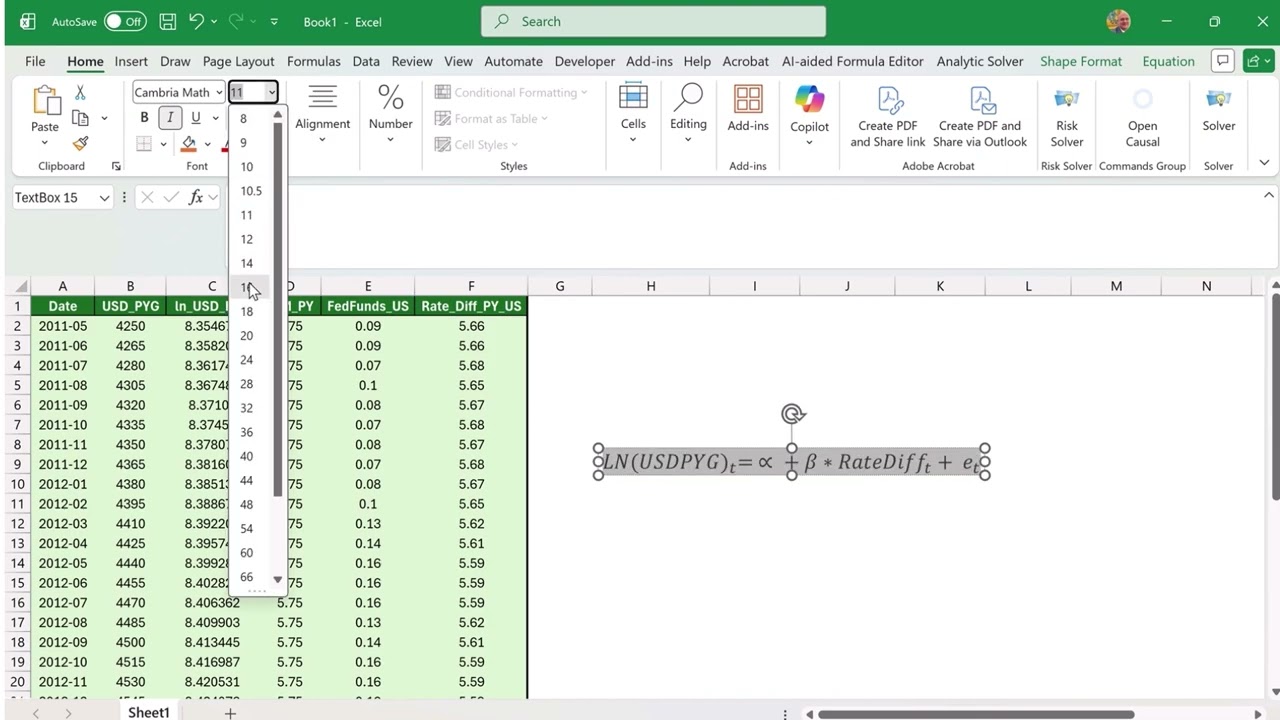

Using monthly data from 2011 onward, the analysis estimates a log-linear regression model in which the logarithm of the USD/PYG exchange rate is explained by the interest rate differential between Paraguay’s monetary policy rate and the U.S. Federal Funds rate.

The estimated results indicate a statistically significant relationship: a 1 percentage point increase in the interest rate differential is associated with an approximate 21% appreciation of the Paraguayan Guaraní against the U.S. dollar. Because exchange rates are modeled in logarithmic form, the estimated coefficient can be interpreted as a percentage effect rather than a level change.

It is important to emphasize that such results should not be interpreted as immediate or mechanical reactions to a single policy decision. In practice, interest rates usually move in increments of 25 or 50 basis points. Based on the estimated coefficient, a 25-basis point change in the interest rate differential would correspond to an approximate 5.3% exchange rate adjustment, while a 50-basis point change would correspond to an adjustment of roughly 10.6%.

These figures should be interpreted as indicative magnitudes over time rather than short-term or instantaneous effects. The interest rate differential likely captures broader monetary conditions, expectations, policy credibility, and capital flow dynamics that unfold gradually. The estimated relationship therefore reflects a longer-run association rather than short-term causality.

In the next video (Part 2), I will extend this analysis by discussing the broader implications of these findings and outlining a future research direction that combines agricultural price indices and interest rate differentials into a single integrated exchange rate model.

Thank you very much for watching. If you found this analysis useful, I invite you to follow the channel for future videos on applied macroeconomics, monetary policy, and exchange rate dynamics in emerging markets.

Доступные форматы для скачивания:

Скачать видео mp4

-

Информация по загрузке: