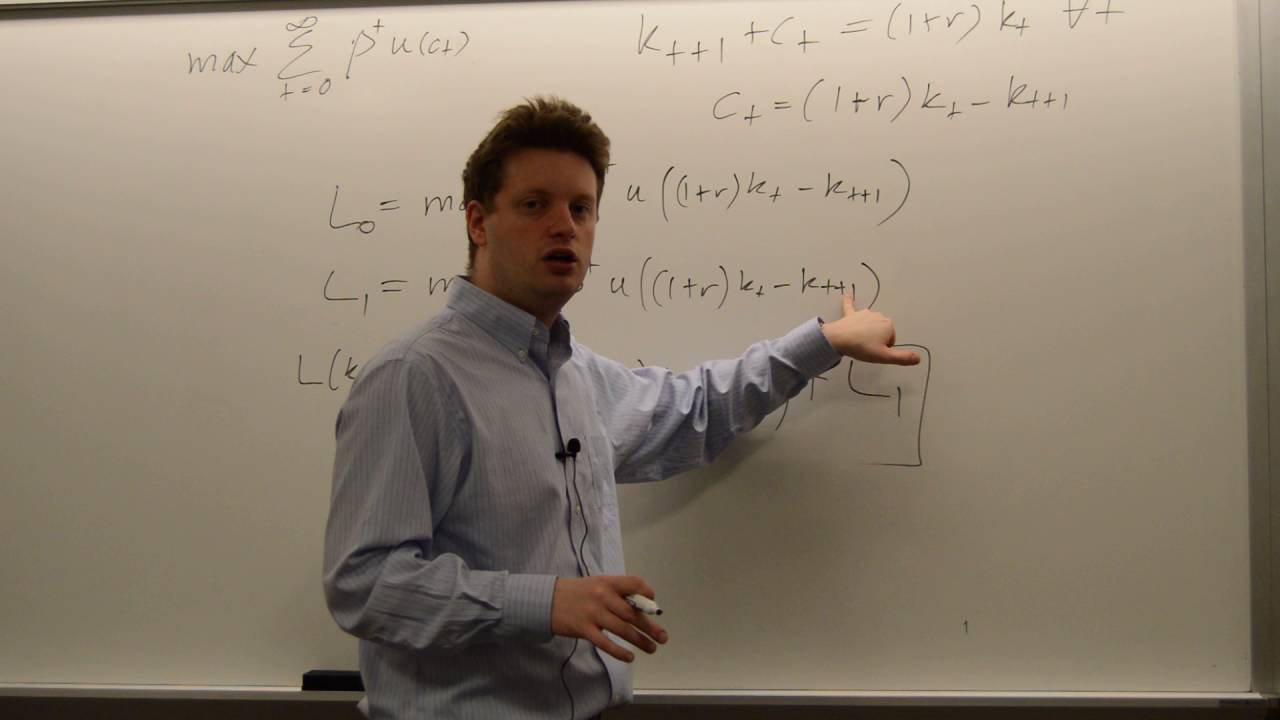

🌿 Dynamic Programming (Finite Horizon) | Bellman Equation & Euler Equation Explained Clearly🌿

Автор: 🌿Mind Maths with Amina🌿

Загружено: 2025-11-24

Просмотров: 63

In this short and focused lesson, we walk through the pure mathematics of a finite-horizon dynamic programming problem. No stories, no travellers problem—just the optimisation setup, the Bellman equation, backward induction, and the derivation of the Euler equation.

What we cover in this video:

✓ The finite-horizon optimisation problem

✓ Setting up the Bellman value function

✓ Understanding the recursion

✓ How the discount factor enters the Bellman equation

✓ Deriving the Euler equation step-by-step

This video is ideal for students of macroeconomics, optimisation theory, or anyone revising dynamic programming in continuous time or discrete time models.

If you find this helpful, don’t forget to like and subscribe for more clear, syllabus-aligned explanations.

#DynamicProgramming #EulerEquation #BellmanEquation #Macroeconomics #OptimizationTheory #FiniteHorizon #EconomicsStudents #MSEconomics #GraduateEconomics #IntertemporalChoice #UtilityMaximization

Доступные форматы для скачивания:

Скачать видео mp4

-

Информация по загрузке: