Скачать

Autocorrelation tests (Part 1): Durbin-Watson statistic (Excel)

Автор: NEDL

Загружено: 2020-07-15

Просмотров: 15940

Описание:

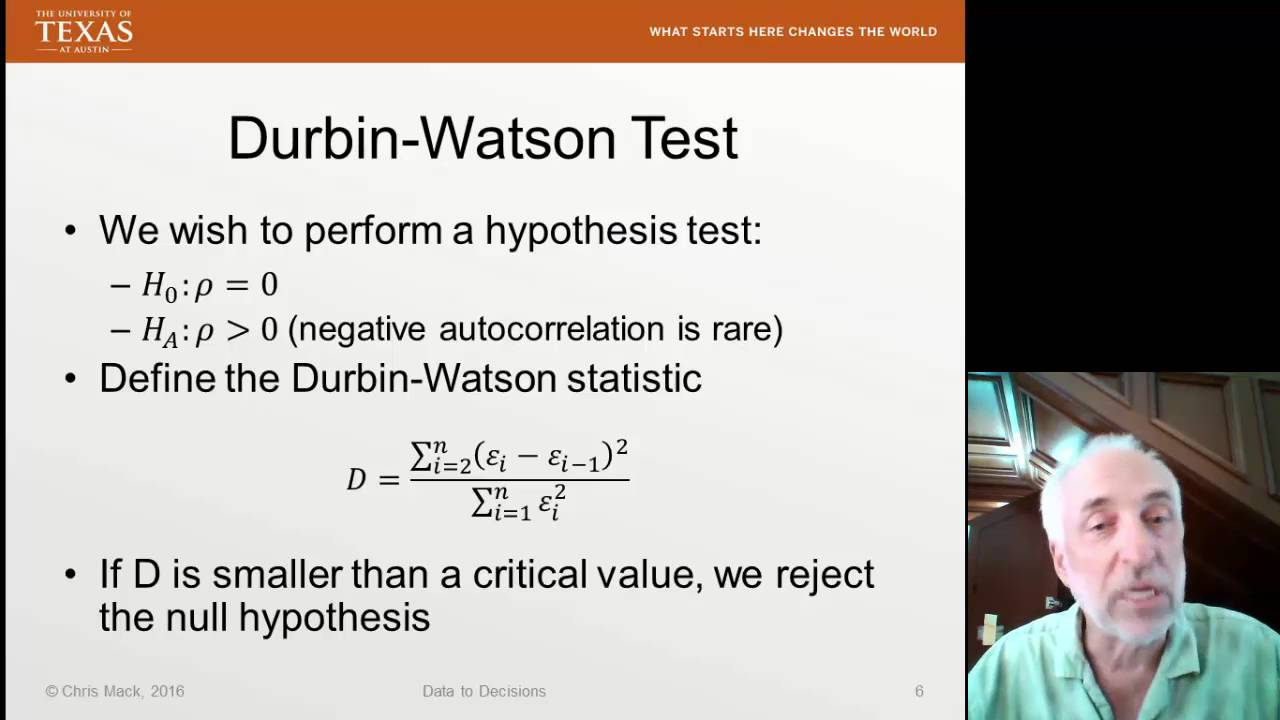

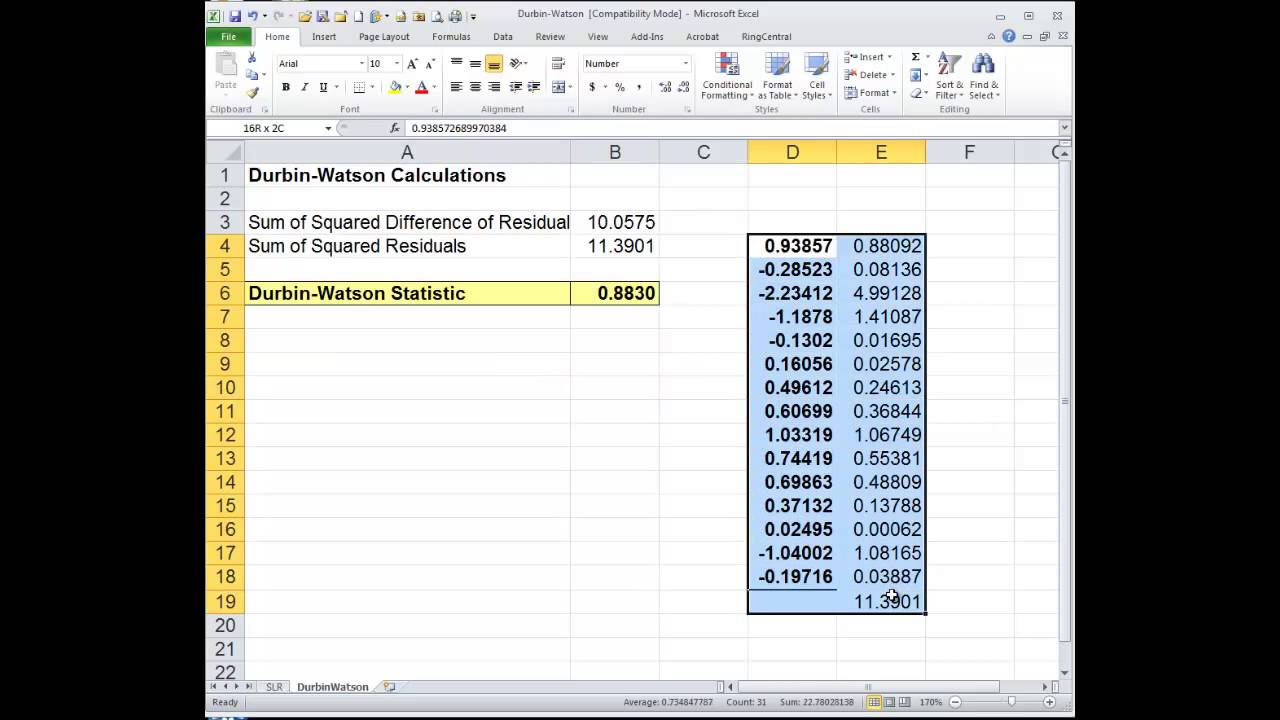

How can one test whether autocorrelation is present in their regression models and if the estimators are therefore biased? The simplest and perhaps most famous autocorrelation testing procedure is the Durbin-Watson statistic. In this video, we are showing how to calculate it in Excel and how to interpret the results, as well as discuss the potential limitations of this approach.

Don't forget to subscribe to NEDL and give this video a thumbs up for more videos in Econometrics!

Please consider supporting NEDL on Patreon: / nedleducation

Доступные форматы для скачивания:

Скачать видео mp4

-

Информация по загрузке: