Brownian Motion for Financial Mathematics | Brownian Motion for Quants | Stochastic Calculus

Автор: QuantPy

Загружено: 2021-09-09

Просмотров: 101549

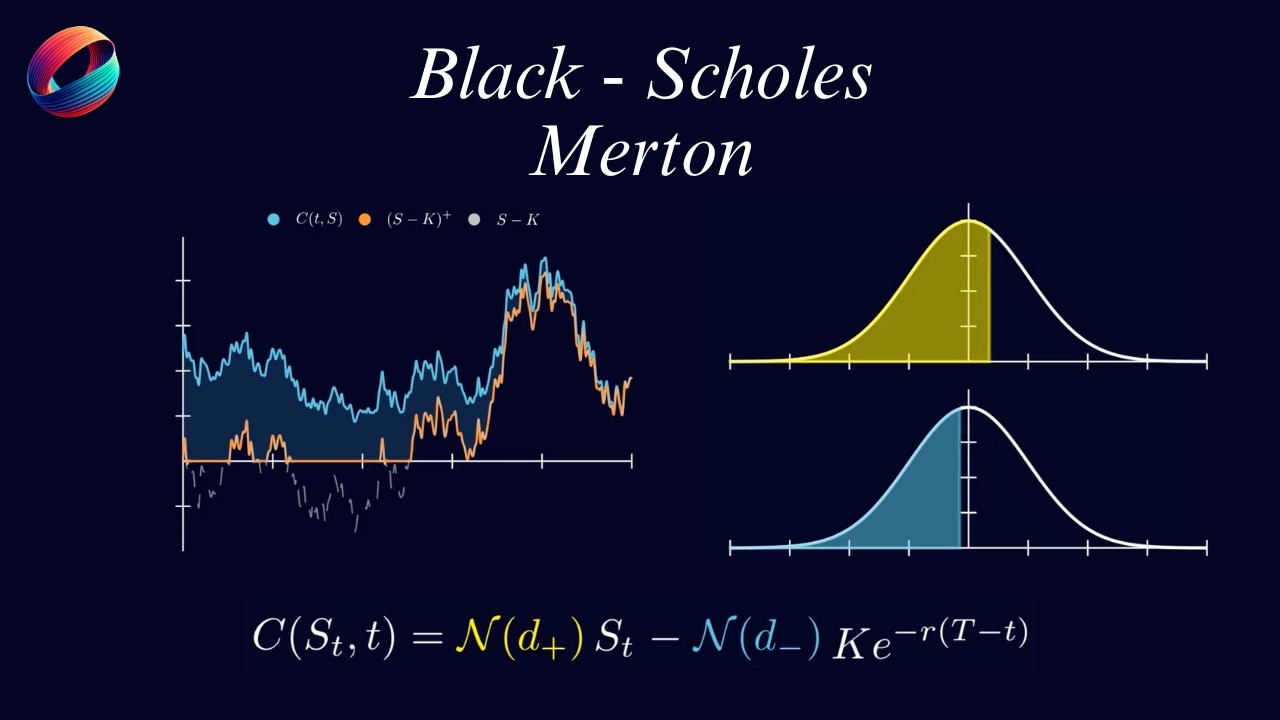

In this tutorial we will investigate the stochastic process that is the building block of financial mathematics. We will consider a symmetric random walk, scaled random walk and Brownian motion. The mathematic notation and explanations are from Steven Shreve's book Stochastic Calculus for Finance II.

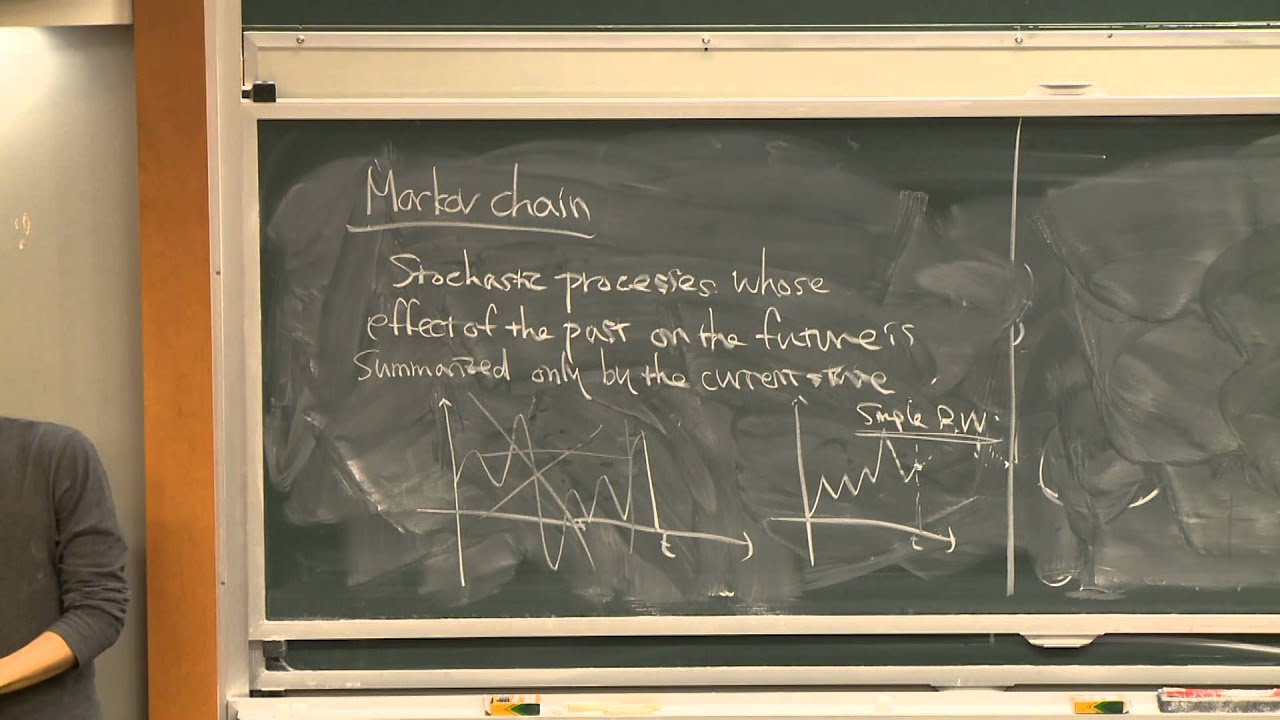

Important properties of Brownian motion are that it is a martingale (Markov process) and that it accumulates quadratic variation at rate one per unit time.

Note: Quadratic Variation is perhaps what makes Stochastic Calculus so different from Ordinary Calculus.

★ ★ Code Available on GitHub ★ ★

GitHub: https://github.com/TheQuantPy

Specific Tutorial Link: https://github.com/TheQuantPy/youtube...

00:00 Intro

02:24 Symmetric Random Walk

06:55 Quadratic Variation

09:08 Scaled Symmetric Random Walk

10:20 Limit of Binomial Distribution

12:10 Brownian Motion

★ A data driven path to getting a job in Quant Finance

https://www.quantpykit.com/

★ QuantPy GitHub

Collection of resources used on QuantPy YouTube channel. https://github.com/thequantpy

Disclaimer: All ideas, opinions, recommendations and/or forecasts, expressed or implied in this content, are for informational and educational purposes only and should not be construed as financial product advice or an inducement or instruction to invest, trade, and/or speculate in the markets. Any action or refraining from action; investments, trades, and/or speculations made in light of the ideas, opinions, and/or forecasts, expressed or implied in this content, are committed at your own risk an consequence, financial or otherwise.

Доступные форматы для скачивания:

Скачать видео mp4

-

Информация по загрузке:

![Цепи Маркова — математика предсказаний [Veritasium]](https://imager.clipsaver.ru/QI7oUwNrQ34/max.jpg)