Stochastic Differential Equations for Quant Finance

Автор: Roman Paolucci

Загружено: 2025-08-12

Просмотров: 14333

🚀 Master Quantitative Skills with Quant Guild

https://quantguild.com

📈 Interactive Brokers for Algorithmic Trading

https://www.interactivebrokers.com/mk...

👾 Join the Quant Guild Discord server here

/ discord

___________________________________________

🪐 Jupyter Notebook

https://github.com/romanmichaelpaoluc...

*Roman's Overview of ODE/PDE/SDEs*

*ODEs*: representing a function as its derivative which can be solved via analytical or numerical techniques to recover said function

*PDEs*: can be constructed using a variety of arguments and used to solve for option prices analytically or numerically (finite-differences)

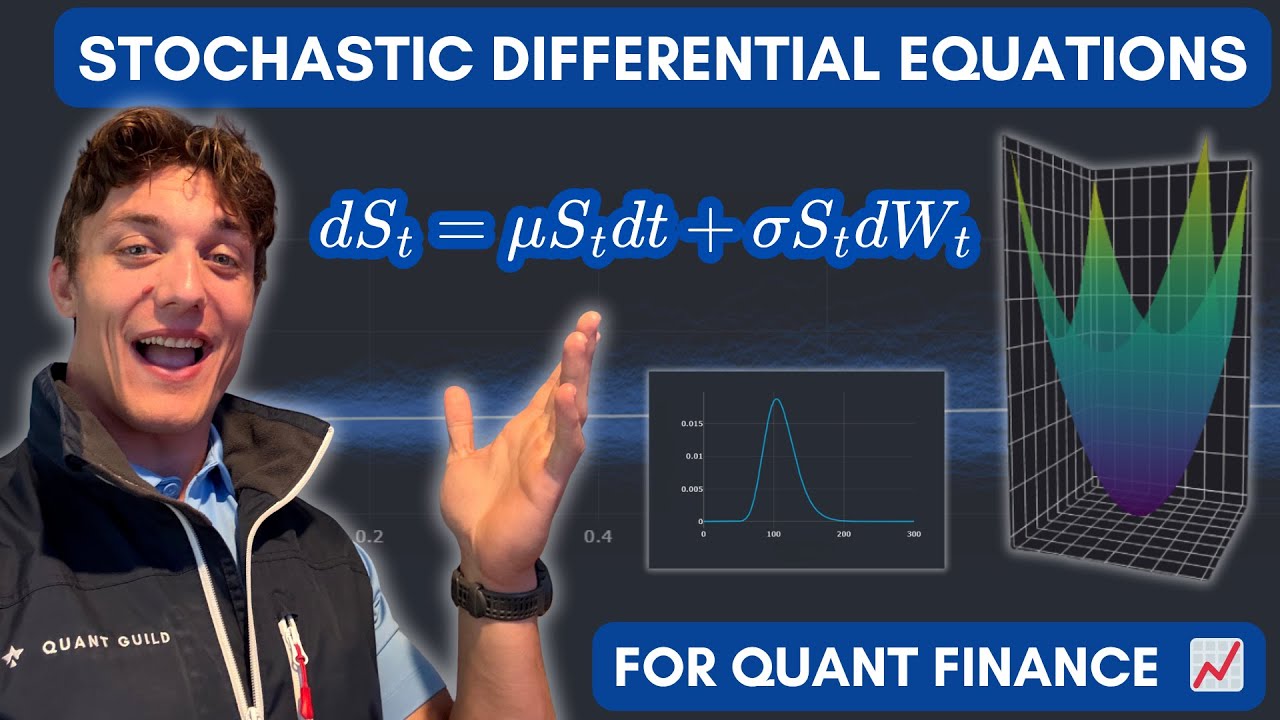

*SDEs*: solutions can be constructed analytically or numerically to produce option prices via the Law of Large Numbers (LLN, Monte Carlo Simulation)

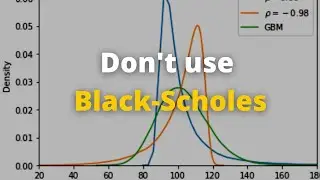

*Black-Scholes Model*: The analytical price is given by the solution to the Black-Scholes equation which can be solved analytically or numerically. The argument assumes a geometric Brownian motion, which can ALSO produce prices via Monte Carlo simulation - I have many videos discussing this idea!

I hope you enjoyed, this was a long one!

Roman

___________________________________________

📖 Chapters:

00:00 - Introduction

02:57 - Understanding Differential Equations (ODEs)

07:15 - How to Think About Differential Equations

09:59 - Understanding Partial Differential Equations (PDEs)

11:31 - Black-Scholes Equation as a PDE

16:49 - ODEs, PDEs, SDEs in Quant Finance

18:17 - Understanding Stochastic Differential Equations (SDEs)

22:30 - Linear and Multiplicative SDEs

23:34 - Solving Geometric Brownian Motion

37:43 - Analytical Solution to Geometric Brownian Motion

40:22 - Analytical Solutions to SDEs and Statistics

43:21 - Numerical Solutions to SDEs and Statistics

47:29 - Tactics for Finding Option Prices

49:46 - Closing Thoughts and Future Topics

___________________________________________

▶️ Related Videos

Ito's Lemma Clearly and Visually Explained

• Ito's Lemma Clearly and Visually Explained

Ito Integration Clearly and Visually Explained

• Ito Integration Clearly and Visually Expla...

Monte Carlo Simulation and Black-Scholes for Pricing Options

• Monte Carlo Simulation and Black-Scholes f...

Why Monte Carlo Simulation Works

• Why Monte Carlo Simulation Works

Expected Stock Returns Don't Exist

• Expected Stock Returns Don't Exist

How to Trade

• How to Trade

How to Trade with an Edge

• How to Trade with an Edge

___________________________________________

🗂️ Resources

📚 Quant Guild Library:

https://github.com/romanmichaelpaoluc...

🌎 GitHub:

https://github.com/RomanMichaelPaolucci

https://github.com/Quant-Guild

📝 Medium (Blog):

/ quantguild

/ quant

___________________________________________

🛠️ Projects

The Gaussian Cookbook:

https://gaussiancookbook.com

Recipes for simulating stochastic processes:

https://papers.ssrn.com/sol3/papers.c...

___________________________________________

💬 Socials

TikTok: / quantguild

Instagram: / quantguild

X/Twitter: https://x.com/quantguild/

LinkedIn (personal): / rmp99

LinkedIn (company): / quant-guild

___________________________________________

Доступные форматы для скачивания:

Скачать видео mp4

-

Информация по загрузке: